What Is the Rent Per Square Foot for Grand Central Office Space?

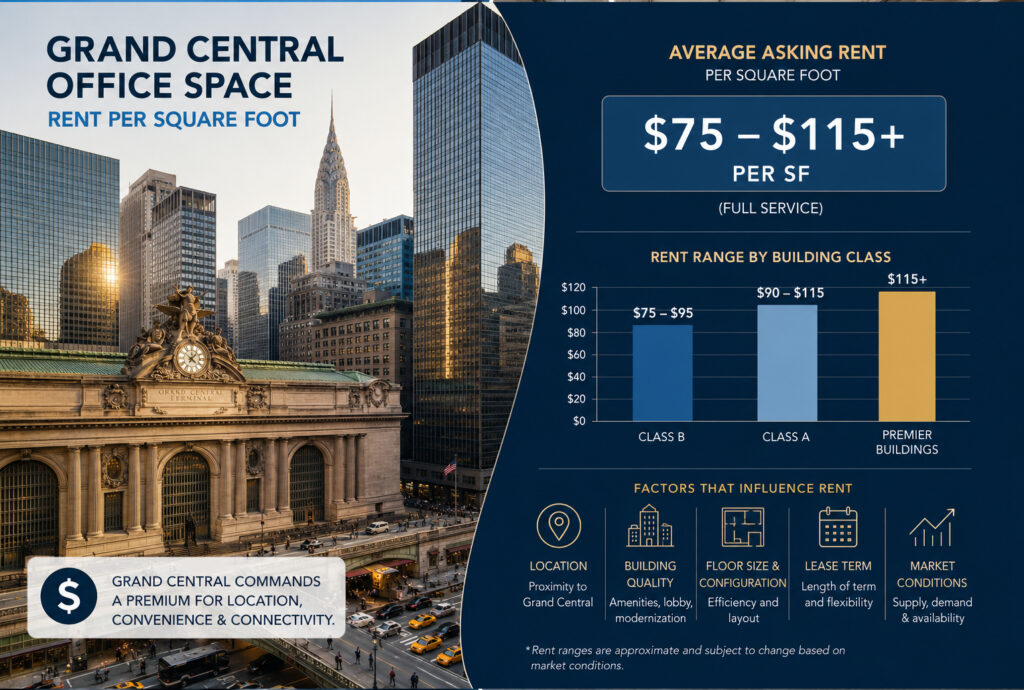

What is the rent per square foot for Grand Central office space? As of spring 2026, the practical tenant answer is that most conventional office users should begin underwriting roughly $70 to $80+ per square foot for the broader Grand Central market, then adjust upward for stronger Class A or Park Avenue product and downward for short-term or value-driven subleases. Cushman & Wakefield places the Grand Central submarket at $69.93/SF overall and $74.18/SF for Class A in Q1 2026, while Savills’ Q1 2026 Grand Central rental-rate comparison places the submarket at $81.21/SF; CBRE’s freshest Midtown read for May 2026 shows $84.77/SF overall and $64.71/SF for sublease space, which is a useful current proxy when you are comparing direct versus second-generation deals.

That band becomes much wider once you move from market averages to live buildings. Current public examples around Grand Central include $105-$115/SF direct space at 100 Park Avenue, $72/SF direct space and a striking $25/SF sublease at 420 Lexington Avenue, a $95/SF marketed suite at 230 Park Avenue, and a $135/SF sublease at 200 Park Avenue. By contrast, 485 Lexington Avenue and One Grand Central Place are currently marketing space on a quote-only basis, even though both have live availability.

For tenants, the key point is that there is no single “Grand Central rent”. There is a market average for budgeting, a different live asking range by building quality, and then a separate effective rent once free rent, TI allowance, electric, furniture, and remaining term are modeled correctly. Savills explicitly notes that its quoted rents are average asking gross rents per square foot and that its statistics use both direct and sublease information, which is one reason different research houses can show different but still useful Grand Central numbers at the same time.

Current Grand Central Rent Benchmarks

If you are budgeting today, the cleanest way to frame Grand Central is as a high-$60s to low-$80s neighborhood benchmark, inside a Midtown market that remains more expensive overall but still offers sublease discounts. Grand Central itself totaled 43.86 million square feet of inventory in Cushman’s Q1 2026 report, with 1.10 million square feet of sublet vacant space, which means sublease opportunities matter, but they are still only one part of the market.

| Benchmark | PSF | What it tells a tenant |

|---|---|---|

| Grand Central overall asking rent | $69.93/SF | Useful baseline for neighborhood budgeting across all classes |

| Grand Central Class A asking rent | $74.18/SF | Good starting point for conventional Class A underwriting near the terminal |

| Grand Central rental rate | $81.21/SF | Higher Grand Central benchmark from Savills’ charted submarket comparison |

| Midtown overall asking rent | $84.79/SF | Broader Q1 comparison point for Grand Central tenants |

| Midtown sublease asking rent | $64.02/SF | Q1 benchmark for second-generation Midtown product |

| Midtown overall asking rent | $84.77/SF | Fresh May 2026 read for current underwriting |

| Midtown sublease asking rent | $64.71/SF | Fresh May 2026 sublease benchmark |

| Manhattan overall asking rent | $73.13/SF | Shows Grand Central is close to borough-wide average on Cushman’s methodology |

| Manhattan Class A asking rent | $83.25/SF | Helpful upper-market reference for stronger product |

Translated into tenant language, current Class A space in and around Grand Central can run from the low $70s into the $100s or more, depending on building quality, build-out, frontage, and prestige. At the more value-oriented end, still-well-located Class B space one block from the terminal is currently being marketed at $55-$60/SF at 52 Vanderbilt Avenue, while stronger Class A examples include $72/SF at 420 Lexington, $95/SF at 230 Park, and $105-$115/SF at 100 Park.

It is also important not to treat $100+/SF pricing as an outlier anymore. JLL’s Q1 2026 U.S. office report said more than 4 million square feet of leasing volume in the quarter was executed at starting rents above $100/SF, the highest first-quarter volume JLL had recorded at that threshold, which helps explain why premium Grand Central addresses can sit far above broad submarket averages.

Live Building Examples Near Grand Central

The averages above are the right place to start, but tenants ultimately sign buildings, not averages. The table below shows what is publicly visible right now in a group of Grand Central buildings that tenants commonly compare.

| Building | Current public asking PSF or status | What is live now | Tenant takeaway |

|---|---|---|---|

| 485 Lexington Avenue | Quote only on current direct space | SL Green is marketing multiple direct blocks from 2,084 SF to 54,199 SF, mostly on 10-year direct terms; CommercialSearch also shows current subleases of 14,566 SF and 28,276 SF expiring in March 2028 | Budget from submarket averages until proposals come in; strong direct-vs-sublease comparison candidate |

| 100 Park Avenue | $105-$115/SF/YR full service | Current live direct spaces include 5,205 SF at $105/SF, multiple 10,889 SF floors at $110/SF, and higher-floor suites at $115/SF | A live example of upgraded Grand Central Class A pricing above submarket average |

| 230 Park Avenue | $95/SF on a marketed 4,260 SF suite; $120/SF reported on a 2026 expansion | A currently indexed 33rd-floor suite is marketed at 4,260 SF / $95/SF, while CoStar reported Helmsley hit $120/SF with StoneX | This is where terminal-fronting prestige starts to push well above the average |

| 420 Lexington Avenue | $72/SF/YR direct on current 16th-floor spaces; $25/SF/YR on a current 3,249 SF sublease | CommercialSearch shows direct Class A space at $72/SF and a live sublease at $25/SF; SL Green’s owner page shows numerous prebuilt direct units on 5-10 year terms | Probably the clearest current example of how wide the direct-versus-sublease spread can be inside one Grand Central building |

| One Grand Central Place | Quote only | ESRT is currently marketing 39,556 SF whitebox and 5,772 SF and 11,590 SF prebuilt suites, all available immediately | Strong direct-lease fallback when you want terminal access but need a bespoke proposal |

| 52 Vanderbilt Avenue | $55-$60/SF/YR full service | Current direct Class B spaces range from 3,797 SF to 9,275 SF; building is updated May 25, 2026 and sits effectively on top of Grand Central | Useful lower-cost comparator if you want location first and trophy image second |

| 200 Park Avenue | $135/SF/YR sublease | Current live 46,143 SF sublease on the 31st floor expires August 31, 2032 | Premium comparator that shows how expensive top-end Grand Central product can get |

What these examples show is that “Grand Central office rent” is really a ladder of product types. Lower-cost but still highly convenient options can sit in the mid-$50s to low-$60s, mainstream Class A can cluster around the low-$70s, stronger Park and terminal-adjacent product can move into the $90s to $115+ range, and premium long-run subleases or high-amenity trophy-like space can push well above that.

How Face Rent Becomes Real Occupancy Cost

For tenants, the most useful formula is still the simplest one: annual base rent = RSF × PSF, and monthly base rent = RSF × PSF ÷ 12. That sounds straightforward, but you should never stop at face rent, because current Grand Central listings show that some spaces are quoted full service, while some buildings still separately flag submetered electric, and others market the value of furniture, prebuilt delivery, or owner-funded build-out instead of publishing a fully transparent apples-to-apples number on the webpage.

| Scenario | Size | Face rent | Annual base rent | Monthly base rent |

|---|---|---|---|---|

| Grand Central overall benchmark | 5,000 RSF | $69.93/SF | $349,650 | $29,138 |

| Midtown sublease benchmark | 5,000 RSF | $64.71/SF | $323,550 | $26,963 |

| 100 Park Avenue mid-ask example | 5,000 RSF | $110.00/SF | $550,000 | $45,833 |

| 420 Lexington current sublease | 3,249 RSF | $25.00/SF | $81,225 | $6,769 |

| 230 Park marketed suite | 4,260 RSF | $95.00/SF | $404,700 | $33,725 |

| 52 Vanderbilt Class B example | 5,000 RSF | $55-$60/SF | $275,000-$300,000 | $22,917-$25,000 |

The headline lesson is that sublease discounts are real, but they are not universal. CBRE’s May 2026 Midtown sublease average of $64.71/SF offers a sensible broad benchmark, yet the live $25/SF Graybar sublease proves that some second-generation opportunities can be deeply discounted when remaining term, condition, or sublandlord motivation line up. At the other extreme, well-positioned Grand Central product can sit at $105-$115/SF at 100 Park, $120/SF at Helmsley on a reported expansion, and $135/SF on a current 200 Park sublease.

A direct lease can also become more competitive than a cheaper-looking building once concessions are modeled correctly. Current owner marketing at 485 Lexington and 420 Lexington explicitly references TIA, new building installation, or prebuilt space, while One Grand Central Place is actively marketing both whitebox and prebuilt suites; those details can materially reduce your real occupancy cost even when the face rent looks higher on day one.

| Sample LOI economics | Illustrative assumption | Amount |

|---|---|---|

| Premises size | Direct lease | 10,000 RSF |

| Face rent | Based on current Grand Central benchmark band | $81.21/SF/YR |

| Lease term | Typical longer direct term | 7 years |

| Annual face rent | 10,000 × $81.21 | $812,100 |

| Gross base rent over full term | $812,100 × 7 | $5,684,700 |

| Free rent credit | 6 months | -$406,050 |

| TI allowance value | $80/SF | -$800,000 |

| Effective base rent after free rent only | ($5,684,700 – $406,050) ÷ 70,000 RSF-years | $75.41/SF/YR |

| Effective base rent after free rent and TI | ($5,684,700 – $406,050 – $800,000) ÷ 70,000 RSF-years | $63.98/SF/YR |

| Effective monthly occupancy cost after those concessions | Net term cost ÷ 84 months | $53,317/month |

This sample is illustrative, but it captures the core point: a face rent around the current Grand Central benchmark can fall by well over $17/SF in effective terms once free rent and TI are properly valued. That is why sophisticated tenants compare face rent, effective rent, and all-in occupancy cost separately instead of focusing on the rent roll headline alone. The face-rent assumption above is anchored to Savills’ current Grand Central benchmark, while the economics of landlord work and prebuilt delivery are supported by the live owner marketing at SL Green and ESRT properties in the district.

How Term, Concessions, and Product Type Change the Deal

The biggest mistake tenants make around Grand Central is assuming that the cheapest quoted PSF is automatically the best deal. In reality, term, delivery condition, and capital responsibility usually matter just as much. A current direct deal may come with owner-funded work, a higher-quality prebuilt, or a more secure long-term position, while a sublease may come with lower face rent, faster occupancy, and existing furniture but less renewal control and less room for TI. Current live inventory around Grand Central shows all of those patterns: 485 Lexington has partially furnished direct inventory and owner-backed installation options, 420 Lexington has prebuilt units and even furniture-available space, and One Grand Central Place currently spans both whitebox and prebuilt product.

For that reason, the right negotiation levers are not just “lower rent.” They are also free rent, TI allowance, turnkey build-out, electric structure, furniture inclusion, restoration obligations, lease commencement timing, and, for subleases, consent timing and remaining term. Grand Central specifically rewards tenants who compare these terms line by line, because current product ranges from smaller value-oriented Class B space at 52 Vanderbilt to materially more expensive Class A product at 100 Park, 230 Park, and 200 Park.

The wider market also supports a nuanced negotiation strategy. CBRE’s Midtown numbers show a persistent spread between overall direct asking rents in the mid-$80s and sublease asking rents in the mid-$60s, while Savills and JLL both point to a quality-driven market where premium assets keep winning. In plain English, you can still find value near Grand Central, but the best-located and best-finished buildings are not pricing like distressed commodity space anymore.

Budgeting Checklist, Timeline, and Tenant Next Steps

Before you sign anything near Grand Central, your budget should separate rent from occupancy cost. The items below are the ones that most often change the real economics of the deal.

| Budget item | What to verify before you underwrite it |

|---|---|

| Base rent | Is the quote full service, electricity included, or separately submetered/direct billed? |

| Free rent | Is it front-loaded, blended, or conditioned on build-out timing? |

| TI allowance or turnkey work | Is there a real dollar allowance, or only a vague promise to “build to suit”? |

| Delivery condition | Whitebox, prebuilt, second-generation, furnished, or partially furnished? |

| Furniture and IT | Are desks, conference tables, wiring, and server infrastructure included? |

| Pass-throughs and building charges | After-hours HVAC, cleaning, supplemental condenser water, freight, and special services |

| Sublease-specific items | Consent timeline, prime lease expiration, extension rights, restoration duties |

| Transaction costs outside rent | Legal fees, architect/test fit, moving, cabling, signage, furniture overage, and security deposit |

That checklist is especially important in Grand Central because current live listings already show how much the economics can move based on non-rent items. 485 Lexington advertises partially furnished space and owner-provided installation options, 420 Lexington markets prebuilt units and furniture-available inventory, and One Grand Central Place spans whitebox and prebuilt availability; those are not cosmetic details, they are budget items.

If you are making a real estate decision now, the most effective next step is to underwrite three lanes at once: a market-average direct lease lane, a discounted sublease lane, and a longer-term premium lane. In practice, that means comparing opportunities such as 485 Lexington, 100 Park, 420 Lexington, 230 Park, and One Grand Central Place against at least one lower-cost comparator like 52 Vanderbilt and one premium benchmark like 200 Park. Doing that gives you a true negotiating position instead of a single-building story.

If you need help evaluating Grand Central economics, we can assist with direct leases, subleases, and office purchases. We do not broker coworking or serviced-office memberships. Our role is to help office tenants compare quoted PSF, effective rent, delivery condition, and long-term flexibility so the final decision is based on the real economics of the space, not just the headline asking rent.

Fill out our 📋 online form or give us a call today 📞 212-967-2061 — let’s find the right office for your business.